The final weeks of the year are when small, strategic financial moves can have a big impact on your taxes and long-term plan. Taking action now may help you enter the new year with clarity and confidence.

Below are five high-impact items I recommend reviewing (and consider acting on) before December 31. If any of these feel overwhelming or you’re not sure where to start, I’m happy to walk through them with you — complimentary.

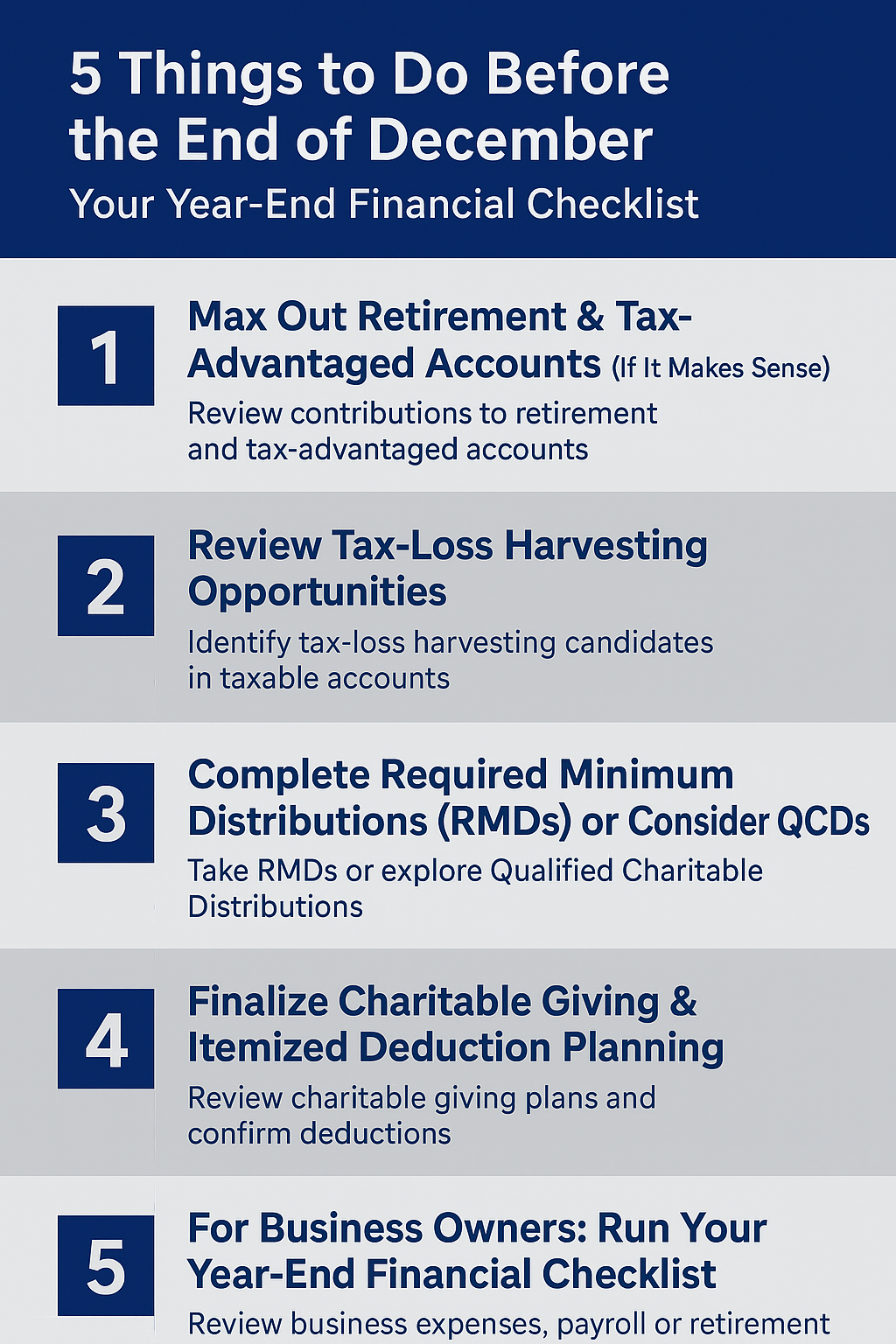

1) Max Out Retirement & Tax-Advantaged Accounts (If It's Appropriate)

Before year-end, review your contributions to:

401(k), 403(b), or other employer plans

IRAs

HSAs

These accounts are some of the most efficient tools available to reduce taxable income and accelerate long-term savings. Many clients are surprised to learn how a small year-end increase in contributions can change their tax picture for the better.

If you’re behind on your goals or eligible for catch-up contributions, this is a great time to close the gap. And if you’re interested in taking advantage of after-tax contributions or mega backdoor Roth options, confirm your plan rules before December 31.

2) Review Tax-Loss Harvesting Opportunities

Tax-loss harvesting allows you to intentionally realize losses in taxable accounts to offset gains or reduce up to $3,000 of ordinary income. This is often a simple year-end strategy that can create meaningful tax savings.

A few reminders:

Keep an eye on wash-sale rules

Make sure your replacement investments keep your portfolio aligned with your long-term strategy

Coordinate with your advisor or CPA to ensure harvesting fits your broader tax picture

A quick review here can deliver significant value, especially during volatile market years.

3) Complete Required Minimum Distributions (RMDs) or Consider QCDs

If you're subject to RMDs, these must be completed by December 31 to avoid steep IRS penalties.

If you’re charitably inclined, you may want to explore Qualified Charitable Distributions (QCDs). A QCD sends funds directly from your IRA to a qualified charity and:

Satisfies your RMD

Reduces your taxable income

Helps support the organizations you care about

Custodians often have cutoffs or processing delays at year-end, so don’t wait until the last week of December.

4) Finalize Charitable Giving & Itemized Deduction Planning

If you give regularly, year-end is the time to revisit your strategy:

Consider bunching charitable gifts to exceed the standard deduction

Verify charities can accept gifts before year-end

Make sure non-cash donations have proper documentation

Confirm all 2025 gifts are submitted and processed by December 31

Thoughtful charitable planning can strengthen your impact while improving your tax position.

5) For Business Owners: Run Your Year-End Financial Checklist

Business owners should review several key items before December 31:

Should you adjust year-end payroll or estimated tax payments?

Do you need to establish a retirement plan for 2025 or make final contributions?

Are there deductions or expenses that should be accelerated into this year?

Are you prepared for tax law changes taking effect in 2025?

A brief review now often prevents bigger issues during tax season — and ensures you’re taking advantage of every available benefit.

You May Also Find This Helpful

For additional strategies to consider, check out my related article:

👉 “5 Money Moves to Make Before Year-End”

Get Your Complimentary E-Book

If you want a deeper dive into common retirement misconceptions — and how to avoid them — request a complimentary copy of my e-book:

👉 Shattering Retirement Myths

Want help prioritizing what matters most for you?

If you'd like help reviewing your year-end opportunities, I’m happy to walk through your numbers and outline actionable next steps.

No pressure — just a complimentary conversation to see if I can provide value.

Schedule a time here!

Sources

Below are the publicly available resources used in researching this post:

Fidelity Investments — Year-End Financial Checklist

Vanguard — Tax-Loss Harvesting and Year-End Tax Planning Guidance

Charles Schwab — RMD and Charitable Giving Rules

IRS — Retirement Plan Contribution Limits & RMD Requirements

BNY / Wealth Management Year-End Planning Insights

Duane Morris LLP — Year-End Tax Planning for Business Owners

Contact Us

For personalized financial planning and asset management services, visit us at one of our convenient locations:

San Diego Office:

5405 Morehouse Drive, Suite 245

San Diego, CA 92121

Irvine Office:

2875 Michelle Dr, Suite 110

Irvine, CA 92606

To schedule a consultation, please call our office at (909) 307-4945 or email us at bradly_stevens@pacificadvisors.com. We look forward to helping you secure your financial future.